Understanding the Current Ratio

The current ratio is a financial metric used to assess a company’s ability to meet its short-term obligations using its short-term assets. It is one of the most widely used measures of liquidity, meaning the ease with which a company can convert assets into cash to pay debts that are due within one year. Investors, creditors, analysts, and managers rely on this ratio to evaluate financial stability, operational discipline, and short-term solvency.

Liquidity is a foundational element of financial health. A company may report strong profits and growing revenues, yet still encounter difficulty if it cannot generate enough cash to satisfy upcoming obligations. Suppliers expect timely payment, employees must be compensated, interest expenses accrue regularly, and tax authorities impose firm deadlines. The current ratio provides a structured method of examining whether available resources are adequate to meet these demands.

Although the metric is elementary in design, its implications extend across corporate finance, credit risk analysis, equity valuation, and internal financial planning. Understanding how to calculate it and how to interpret it in context is essential for anyone engaged in evaluating a company’s financial position.

Definition and Formula

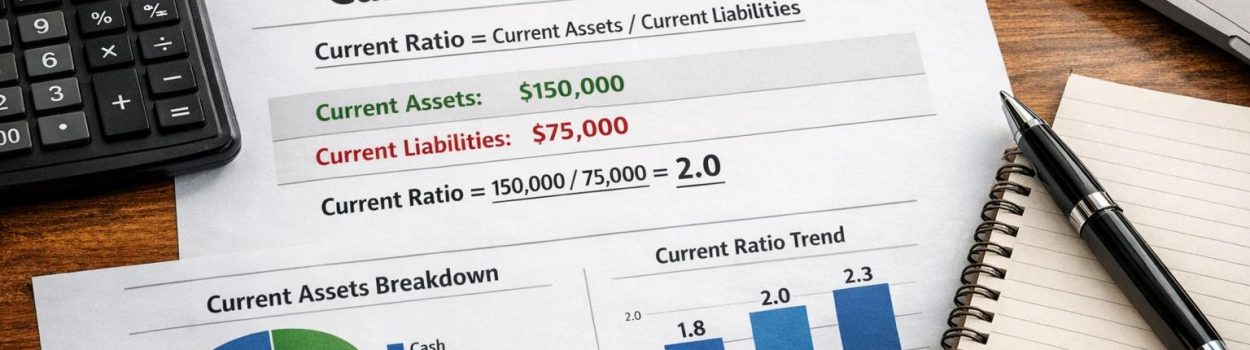

The current ratio measures the relationship between a company’s current assets and its current liabilities. The formula is expressed as:

Current Ratio = Current Assets ÷ Current Liabilities

Current assets consist of resources expected to be converted into cash, sold, or consumed within one year or within the normal operating cycle of the business. Current liabilities represent obligations due within the same period.

If a business reports $800,000 in current assets and $400,000 in current liabilities, its current ratio would be 2.0. This indicates that it has two dollars of short-term assets for every dollar of short-term obligations.

The ratio does not indicate how quickly each asset can be converted to cash, nor does it measure the timing of each specific liability. Instead, it provides a broad picture of short-term solvency at a specific reporting date, usually the end of a fiscal quarter or year.

Components of Current Assets

The precision of the current ratio depends on the proper classification and valuation of current assets. These assets typically include cash and cash equivalents, accounts receivable, inventory, marketable securities, and prepaid expenses.

Cash and cash equivalents are the most liquid resources on the balance sheet. They include physical currency, checking and savings account balances, and short-term instruments such as treasury bills with maturities of three months or less. Because they are immediately available, they represent the strongest form of liquidity.

Accounts receivable arise when a company sells goods or services on credit. These balances are expected to be collected within the credit period, often 30 to 90 days. The reliability of receivables depends on customer quality and credit policies. Slow-paying or financially unstable customers reduce the effective liquidity of this asset category.

Inventory includes raw materials, work-in-progress goods, and finished products available for sale. Inventory liquidity depends on turnover rates, demand conditions, and storage considerations. Goods that sell quickly and require minimal discounting contribute more effectively to liquidity than specialized or obsolete items.

Marketable securities are investments in short-term financial instruments that can be readily sold in public markets. Their liquidity depends on market depth and price stability.

Prepaid expenses, such as advance insurance payments or prepaid rent, are recorded as current assets because they represent future economic benefits within the current year. However, they cannot be converted back into cash and therefore offer limited support in meeting liabilities.

Each category contributes differently to liquidity strength, and analysts often evaluate their composition in detail rather than relying solely on the aggregate total.

Components of Current Liabilities

Current liabilities consist of obligations that must be settled within one year or within the operating cycle. These obligations reflect the company’s short-term financing structure and operational commitments.

Accounts payable represent amounts owed to suppliers for goods and services purchased on credit. Payment terms may range from 30 to 90 days. Efficient payment scheduling can improve liquidity management without disrupting supplier relationships.

Short-term debt includes bank overdrafts, revolving credit facilities, and other borrowings due within one year. These instruments provide flexibility but also require careful monitoring to avoid refinancing risk.

Accrued expenses encompass wages payable, interest payable, and taxes owed but not yet paid. These amounts accumulate over time and must be settled according to contractual or statutory deadlines.

The current portion of long-term debt reflects principal repayments due within the next twelve months on multi-year loans or bonds. Although classified as current, these obligations may have been structured years earlier, and their upcoming installment increases short-term pressure.

Accurate classification of these liabilities is critical because any understatement can make the company appear more liquid than it actually is.

Interpreting the Current Ratio

The interpretation of the current ratio depends on magnitude, trend, and business environment.

A ratio of 1.0 indicates parity between assets and liabilities. In theory, the company can meet all short-term obligations by converting its assets into cash. However, in practice, asset liquidation may not occur at full book value or within the required time frame.

A ratio above 1.0 indicates a surplus of current assets relative to liabilities. Many analysts consider a range between 1.5 and 2.0 to represent balanced liquidity in stable industries. This range suggests a buffer without excessive idle resources.

A ratio significantly above 2.5 or 3.0 can imply underutilized assets, especially if large cash balances generate minimal returns. Such a condition may indicate conservative management or a lack of investment opportunities.

A ratio below 1.0 suggests that liabilities exceed assets. While this may signal liquidity risk, it is not necessarily problematic for companies with rapid cash turnover, predictable revenue streams, or access to revolving credit facilities.

Context, business model, and historical patterns all influence interpretation.

Industry Differences

There is no universal benchmark suitable for every sector. Business characteristics shape liquidity needs and determine acceptable ratio ranges.

Retailers typically maintain fast-moving inventory and receive payments at the time of sale. Consequently, they often operate with lower current ratios while still maintaining sufficient liquidity.

Manufacturing firms must purchase raw materials, sustain production cycles, and hold finished goods before sale. These processes tie up capital in inventory for extended periods. As a result, higher current ratios are often appropriate.

Construction companies may experience uneven cash flows tied to project milestones. Agricultural businesses operate seasonally, which can distort year-end balances. Technology companies may carry limited inventory but large receivable balances.

Therefore, comparing a company to its direct peers yields more meaningful insight than cross-industry comparisons.

Advantages of the Current Ratio

One advantage of the current ratio is its clarity. The required data appear directly on the balance sheet, making computation straightforward.

The ratio provides a quick assessment of short-term solvency, useful in credit evaluations and preliminary investment analysis. Suppliers may use it to determine whether to extend payment terms. Banks often include it in lending assessments and credit scoring models.

Internally, financial managers monitor the ratio to maintain liquidity thresholds aligned with corporate risk tolerance. It also serves as a communication tool, enabling stakeholders to understand liquidity in numerical terms.

Because of its simplicity and accessibility, the current ratio remains a standard metric despite the availability of more complex analytical techniques.

Limitations of the Current Ratio

Despite its strengths, the ratio has structural limitations.

It is based on accounting values rather than market values. Financial statements reflect historical cost conventions, which may not represent realizable cash values in distressed scenarios.

The ratio also measures a single date. A business may temporarily improve its ratio before reporting periods by accelerating collections or deferring payments. Such actions may not reflect sustainable liquidity.

Another limitation lies in asset quality differences. Slow-moving inventory and doubtful receivables weaken true liquidity, yet they remain included at book value.

The ratio does not measure cash flow timing. A company could have a current ratio above 1.5 but still encounter short-term cash shortages if liabilities mature before receivables are collected.

Therefore, analysts often supplement it with additional ratios and cash flow analysis.

Relationship to Other Liquidity Ratios

To obtain a more refined perspective, analysts compare the current ratio with related indicators.

The quick ratio excludes inventory and prepaid expenses, focusing on assets that can be converted to cash more rapidly:

Quick Ratio = (Current Assets − Inventory − Prepaid Expenses) ÷ Current Liabilities

This measure provides insight into liquidity without reliance on inventory sales.

The cash ratio considers only cash and cash equivalents relative to current liabilities. It represents the most conservative liquidity test, assessing whether immediate cash resources could cover obligations without asset sales or collections.

Together, these ratios form a tiered evaluation of liquidity quality and resilience.

Working Capital and Operational Efficiency

The current ratio is directly linked to working capital, defined as:

Working Capital = Current Assets − Current Liabilities

Positive working capital indicates that current assets exceed liabilities. However, the ratio reveals proportional coverage rather than the absolute surplus amount.

Efficient working capital management involves balancing inventory levels, accounts receivable policies, and payment terms. Shortening collection periods reduces receivables balances while increasing cash. Optimizing inventory reduces storage costs and obsolescence risk.

Companies must align these policies with operational needs to maintain smooth production and customer service without creating unnecessary liquidity strain.

Strategic and Financing Considerations

The structure of short-term versus long-term financing influences the current ratio. Firms that rely heavily on short-term borrowings may report lower ratios due to higher current liabilities. Alternatively, companies that refinance short-term debt into long-term obligations can improve the ratio without altering total debt.

Strategic acquisitions, capital expenditures, or expansion initiatives can temporarily alter liquidity. During growth phases, companies may accept lower ratios while expecting future revenue gains.

Dividend policies and share repurchases also affect current assets, particularly cash balances. Decisions in these areas reflect management priorities and risk assessments.

Role in Credit and Investment Analysis

Credit analysts emphasize the current ratio when assessing repayment capacity. Loan agreements frequently include minimum liquidity requirements. If a company breaches these covenants, lenders may demand corrective action.

Equity investors consider the ratio within broader valuation frameworks. Excess liquidity may signal strong risk control but also potential inefficiency. Conversely, limited liquidity combined with consistent free cash flow may indicate disciplined capital management.

Trend analysis often provides more insight than single-period observation. A steadily declining ratio may point to rising leverage or increasing operational strain.

Macroeconomic Influence

Economic conditions shape liquidity management practices. In periods of credit abundance and low interest rates, companies may operate with narrower liquidity margins. Access to revolving facilities reduces the need for large asset cushions.

During economic contractions, firms often strengthen liquidity positions, increase cash holdings, and reduce exposure to short-term debt. Delays in customer payments and supply chain disruption amplify liquidity risk.

Inflation may also distort asset valuations. Rising prices increase inventory values and receivable balances, which can inflate the ratio without necessarily improving real purchasing power.

Understanding broader economic context aids accurate evaluation.

Extended Practical Illustration

Assume a distribution company reports the following balances:

Cash: $150,000

Accounts Receivable: $250,000

Inventory: $400,000

Marketable Securities: $50,000

Prepaid Expenses: $25,000

Total Current Assets: $875,000

Accounts Payable: $300,000

Short-Term Debt: $200,000

Accrued Expenses: $75,000

Total Current Liabilities: $575,000

The current ratio equals:

1.52 = $875,000 ÷ $575,000

A ratio of 1.52 indicates moderate liquidity coverage. However, a deeper review might reveal that inventory turnover is slow, or that a portion of receivables is overdue. Adjusting for these factors could reduce effective liquidity below the reported figure.

Such analysis illustrates the importance of examining both quantitative results and qualitative conditions.

Conclusion

The current ratio remains one of the most established measures of short-term financial stability. By comparing current assets to current liabilities, it provides a structured method for assessing whether a company can meet obligations due within one year.

Although simple in formula, interpretation requires consideration of asset composition, liability structure, industry norms, working capital efficiency, and economic environment. The ratio should be evaluated over time and alongside complementary liquidity measures such as the quick ratio and cash ratio.

When applied carefully and in context, the current ratio contributes to informed judgments regarding creditworthiness, operational resilience, and financial management effectiveness within trading, brokerage, and broader corporate environments.